- Starting a business is not about timing as much as it is about learning and growing, even if your first idea fails.

- Business survival rates are low but it doesn’t matter if the economy is growing or in recession.

- The key is having accounting skills, cash management and knowing your customer.

You could start a business today. Many now huge firms started with just a conversation and a decision.

And while starting a business is never a time to look without leaping, at some point you must take that first big step.

There will never be a perfect or prime moment in your life to start a business. You shouldn’t fear failure, give in to procrastination or wait for the “right” moment to come along.

However, it is good to obsess over doing what realistically needs to be done to achieve success, rather than just obsessing about success. Don’t lose the forest for the trees that way.

Henry David Thoreau once said that the inspiration outweigh any concern with success.

“Success usually comes to those who are too busy to be looking for it,” he wrote.

No business can succeed without hard work or a strategy. You need an operations strategy and a business plan.

But waiting for the right moment might mean waiting forever. Instead, start a business today.

Is your goal to start a business today?

Even with all of the information in the world, some people can panic or immobilize themselves with fear.

Start simply. Take a piece of paper and plot what kind of business you want and what you want to do. Ask yourself these questions:

• What is your business?

• What service will you offer?

• Do you enough financing to start and maintain your business for a year or more?

• Who is your consumer?

• Can you handle the logistics, recordkeeping and accounting required to run a business?

• Will you be a nonemployee business, a sole proprietor, or will you have employees?

This is just a sampling of the questions that you should ask yourself before you start your own business. Getting lost in the questions is not the point.

Rather, it’s about answering these self-directed questions in a realistic way to justify and plot the launching of your business.

You can do this. Who you are and your age need not be a deterrent. According to research from Small Business Trends, more than 51% of business owners are between the age of 50 and 88. About 33% of business owners are between the ages of 35 and 49.

Only 16% of business owners are aged 35 or under.

Start small. Consider the startup costs. Know your consumer. Know that you can benefit from traditional and digital marketing, no matter how small the business. Learn from your mistakes as you go along.

Have strategic and situational awareness of the financial and business environment that you are living in. Assess how you should strategically launch your business.

Be aware of the consequences of failure though you shouldn’t let it deter you. Be realistic. Then go for it and start a business today.

Business survival odds

A bitter reality of business life in the United States is that most businesses fail within two to five years of launching.

A lot of businesses in the United States fail before they can recoup costs, make a profit, sustainably market themselves or create a consumer-trusted brand.

Yet the survival rate for most new businesses plateau considerably upon launching after a few years.

According to the Small Business Administration, about 20% of all new businesses fail within a year. About 34% of all businesses fail within the second year.

Think about that, however. Within two years of launching, a little more than six out of 10 new businesses have a statistical chance of succeeding.

After half a decade about half of new businesses fail. After 10 years, over 70% of new business fail in the United States.

That means that a decade after launching only three out of 10 new businesses are still in business.

It doesn’t matter what industry your new business may represent. The first few years of operation are always the hardest. However, the longer that you stay in business, the likelier that you will stay in business.

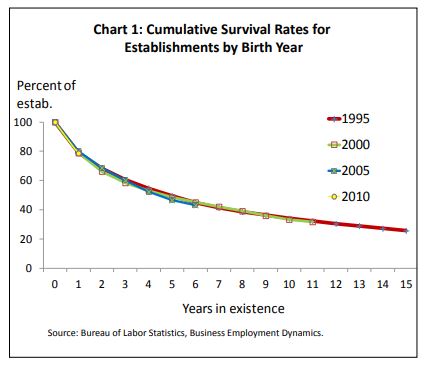

It is also good to remember that the survivability odds for a new business have little to do with the robustness of an economy. By that measure, timing is not everything.

As per research conducted by the Bureau of Labor Statistics and Business Employment Dynamics, new businesses launched before and years after the 2008 global financial crisis experienced near similar survival trajectories.

In good times and in bad times, consumers consume. It won’t matter if you start a business today or next year in terms of the economy.

These statistics are not meant to dissuade you from launching your own business. It’s very easy to become discouraged. It’s all about being realistic about knowing exactly what you are getting yourself into before you start.

So let’s examine some of the reasons why new businesses fail.

Cash flow problems

A U.S. Bank research report finds that more than 82% of new businesses fail because of constant internal cash flow problems. Basically, poor money management skills.

A study by Visual Capitalist reveals that more than 29% of new businesses fail because they run out of money.

According to Small Business Trends, only about 40% of new startup businesses are ever profitable. About 30% of new businesses just continually break even.

That is, they make just enough money to continue operations, but never really profit. About 30% of businesses steadily lose money during operational existence.

When you start a business, it might be practical to hire a bookkeeper, accountant or lawyer. If you don’t know what you are doing you could easily make money but also lose money at the same time.

It helps to know the difference between revenue and profit, which are not the same thing.

Revenue is all the money your business generates from different sources. Profit is whatever remains after all the bills have been paid.

The cash your business generates should continually be reinvested back into your business. You must keep accurate books and pay attention to detail. If you don’t, you could just be feeding a self-perpetuating money pit.

Think about expenses. If you rent an office or space for your business, you must pay rent and utilities. You have to pay salary if you have employees. You will need to pay for insurance, taxes and other fees.

If you start a business that requires inventory, then that is an expense that must be turned into a profit. The longer that inventory sits on the shelf of a business, the longer it will take to make money.

When you do business with vendors, suppliers and other businesses, it could take weeks or months to be paid via invoicing. You must budget accordingly so you don’t experience significant gaps in cash flow before getting paid.

If your monthly or annual profits are constantly less than what you pay in expenses, that is a recipe for failure.

You could start a business today and be making just enough money to pay your expenses but not necessarily enough to stay in business for long.

Learn from mistakes

Running a business is more complicated than the few examples just presented. It is not impossible either.

You must always be aware of the money coming in versus those going out. Timing and strategy are everything when you want to increase profits.

Discouraged yet? Well, you shouldn’t be at all. In fact, you are just as likely to succeed in business after a failure as opposed to never trying. As long as you are realistically determined, there is no reason not to try.

More than 20% of people who failed in a previous business succeed in their next venture. About 18% of first time businesspeople are successful.

Failure, and learning acutely from such, can be one of life’s greatest teachers, especially failure in business.

Now that we have discussed the realities of business survivability, lets discuss how you can realistically start a business.

Start-up capital

You should have a strategy, business plan vision and, optimally, an accountant when you launch a business.

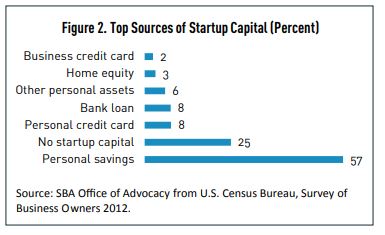

Consider that most big things start off in very small ways. Over 82% of all new business owners self-financed their own launches.

As per studies conducted by the SBA and Wells Fargo, the average new business needs anywhere between $10,000 to $80,000 in startup capital.

How much money you make isn’t a barrier to starting a business either. According to Payscale, the average low-to-medium annual salary range of a new business owner is between $26,614 and $59,667.

Acquiring a business loan from an investor or financial institution depends on how much money and collateral you have on hand. It is in your best interests to develop a detailed business plan, with the help of a professional if possible.

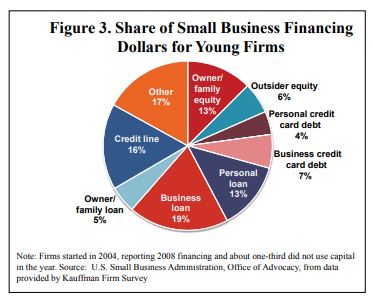

The SBA reports that more than $600 billion in small business loans were granted in the United States in 2015. Only about 8% of new businesses launched via a bank loan or with credit cards.

Additionally, more than 73% of new businesses made use of some sort of financing within the last year.

The point is that if you have a dream of starting a business today, you don’t need as much money as you think to make it a reality.

How much money you need does not matter as much as how you use it on your business. Take the time to plan how your business will run and how it will make money.

Big things start in small ways

According to Small Business Trends, almost 69% of all new, small businesses begin as a home-based endeavor. Moreover, more than 59% of new businesses continue to operate from their original home base.

You can start out as an independent contractor, sole-proprietor or non-employee business. You can hire employees, if needed, as your business grows.

There are about 30 million small businesses operating in the United States employing about 57 million people. Some of these companies employ as little as 20 people.

In fact, over 99.7 of all the businesses in the United States are small business employing less than 500.

Small businesses are the engine of the American economy, from the sole proprietor to the 500 employee firm.

Its not the size of the business that matters. The determination of the owner is all that matters.

If you can responsibly raise anywhere between $10,000 and $80,000 to launch a business, go ahead and start a business today.

Know your consumer

Starting a new business is no easy task. Still, even the smallest home-based business must conduct research into their proposed consumer base or demographic.

Who are your consumers? Why will they buy your product or service? Most important, why would they buy your product or service over an establish competitor?

You should always keep a situational awareness of market conditions and competitor activity.

About 19% of new business launches fail because they don’t differentiate from their competition. Another 42% of businesses fail because they discover the hard way that there is no market or demand for their product or service.

You shouldn’t just market to any consumer. You should market to your consumers.

Along with traditional marketing, make the most of email and social media. Send out advertisements and newsletters with a questionnaire to gauge consumer needs. This way you can build a database of clients.

Tailor your advertising for optimization via smart devices. According to eMarketer, about 51% of people globally interface with the Internet via smartphone. That’s about 2.56 billion people.

That figure is primed to trend upward in the future.

Additionally, you can conduct preliminary business demographic research through the SBA, Bureau of Labor Statistics and the United States Census Bureau.

Yes, you can start a business today

Look as much as possible. At some point though, you must take that first step.

These rudimentary guidelines are just the start of the things you must consider before starting a business. Make a business plan. Consider your goals, your product or service and your potential consumer.

Make a list of questions concerning your business. Consult with a lawyer, financial expert or a successful business owner. Strategize and plan.

There will never be a perfect moment to start your business. You could start a business today, or wait. It won’t matter in the long run.

Good or bad economic times won’t affect your business’ survival as much as you think. A recent Wall Street Journal report cites economists’ concerns that the next American recession will begin in 2020.

In good times or bad times, however, consumers consume. So, ask yourself one question: What can you offer as a businessperson?

The only thing harder to live with in life besides failure is regret. Besides, two of out 10 successful startup businesses were born out of a previous failure.

Take that first step and start a business today. It won’t be easy. You might fail and learn something that will be worth it.