Wondering when to take Social Security? Take a peek at the Social Security Administration calculator.

Benefit estimates depend on your date of birth and your earnings history.

For security, the Quick Calculator does not access your earnings record; instead, it will estimate your earnings based on the information you provide. So benefit estimates made by the Quick Calculator are rough.

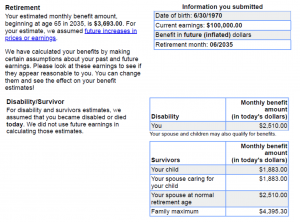

For example, let’s say you were born on June 30, 1970, with current earnings of $100,000 and you were looking to retire at age 65, June 30, 2035.

Here is a sample of the resulting retirement benefits:

If you have a My Social Security account, you can get the most accurate estimate there. If you don’t have an account you can create one.

Goals

Are your current retirement planning strategies generating enough funds for you to meet your retirement goals?

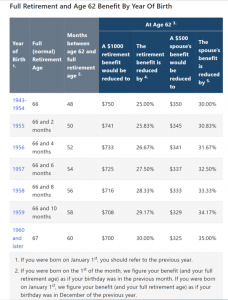

You have the option to take retirement benefits as early as age 62. However, so-called “full” retirement benefits are payable at age 67.

If you or delay collecting your retirement benefit until age 70, it will be for a higher monthly amount.

It amounts to an 8% “raise” every year you wait after your full retirement age, which varies by birth year. There is no incentive to delay claiming after age 70.

While it might seem like a bad deal to start taking benefits early remember, those who do are likely to collect checks for longer.

The government doesn’t reward you for starting Social Security payments early, on time, or late. It’s the same total estimated payment regardless of the time frame you choose.

The million-dollar question is how long will you live, and do you want a reduced amount for more years or higher amounts for fewer years.

The chart below, from the Social Security Administration, breaks it down in detail.

Besides your likely longevity, what also matters is your financial needs, current health condition, and if you enjoy working or not.

The best thing you can do to help with retirement planning is to hire a certified financial planner (CFP) and have them put together a custom financial plan based on your current assets, liabilities, as well as needs, wants, and wishes.

He or she will have you fill out a detailed questionnaire so that they can better understand how you live today and how you want to live in the future.

Most advisors today use financial planning software because it provides sophisticated solutions and smart assumptions to help advisors navigate the complex financial elements of their client’s lives.

The main focus of these programs is around:

- Retirement planning

- Tax planning

- Retirement savings and income planning

- Estate planning

- Investment planning

To find a CFP near you, use the group’s website. You can search by zip code.

The CFP certification is the standard of excellence in financial planning. CFP professionals are required to meet rigorous education, training, and ethical standards, and are committed to serving their clients’ best interests today to prepare them for a more secure tomorrow.

If you don’t want to pay for professional help or feel that your needs are simple, you can visit the Social Security Administration directly and learn more about retirement planning and the benefit credits you have accumulated over the years.

In any case, it helps to have a clear, written projection of your benefits and to understand the advantages and disadvantages of different claiming ages.